Portfolio and Arbitrage

The mathematical theory of financial markets often begins with single-step discrete models that capture the fundamental ideas to build more complex models at both discrete and continuous time levels. It is also important to establish precise mathematical notations for familiar financial terms such as portfolio and arbitrage opportunity, which are essential for developing fair pricing or risk-neutral models.

In this chapter, we introduce the mathematical notions of portfolios, their values, and gains through which we establish a precise language for modelling market activities. We further give a general framework for building probability models that represent market uncertainty in a single time step that forms the foundation for more advanced multi-step models. An important concept explored in this chapter is arbitrage, which is a cornerstone of modern financial theory that ensures consistency in pricing and market equilibrium. As an application, we derive the forward pricing model and demonstrate how these concepts provide practical insights into real-world financial instruments.

Section «Click Here» establishes essential mathematical notations and defines, for a portfolio, its value and its gain. Additionally, this section illustrates the idea of constructing a probabilistic model for a finance market. Section «Click Here» introduces an important concept of derivative pricing, the arbitrage opportunity and its applications in developing forward and future pricing models.

Portfolio Concepts

We denote a collection of securities with deterministic cashflow (such as bonds and bank accounts) by

and a collection of risky securities (such as stocks) by

A capital market (also referred to as spot market or underlying market in the context of derivatives) is a collection of assets \(\big(\boldsymbol{B},\boldsymbol{S}\big)\).

A collection of derivative securities

is a derivatives market.

A market is a collection of securities \((\boldsymbol{B}, \boldsymbol{S},\boldsymbol{H})\).

Mrs. Sahana has a surplus of ₹ 1,00,000, which she kept in her savings account at a bank, intending to invest the money in the stock market. She selected her five favorite stocks \(\boldsymbol{S}=(S^{(1)}, S^{(2)}, \ldots, S^{(5)})\). For instance, \(S^{(1)}\) represents TCS, \(S^{(2)}\) represents SBI bank, \(S^{(3)}\) denotes Reliance, \(S^{(4)}\) corresponds to Infosys, and \(S^{(5)}\) corresponds to Bajaj Auto. Then, she considered her own model market \((B, \boldsymbol{S},\boldsymbol{H})\), where \(B\) represents her savings account, which pays interest at the rate of 4% per annum compounded quarterly and \(\boldsymbol{H}\) represents the corresponding derivatives.

Once a market is fixed, a portfolio can be defined as a mathematical representation of the quantities of different assets held in the market.

A portfolio of a given market \((\boldsymbol{B},\boldsymbol{S},\boldsymbol{H})\) is an ordered \((n_b+n_s+n_h)\)-tuple of real numbers

where \(\boldsymbol{\phi}=(\phi^{(1)},\phi^{(2)},\ldots,\phi^{(n_b)})\) with \(\phi^{(i)}\) being the number of units of the asset \(B^{(i)}\), \(i=1,2,\ldots,{n_b}\), \(\boldsymbol{\theta}=(\theta^{(1)},\theta^{(2)},\ldots,\theta^{(n_s)})\) with \(\theta^{(i)}\) being the number of units of the asset \(S^{(i)}\), \(i=1,2,\ldots,n_s\), and \(\boldsymbol{h}=(h^{(1)},h^{(2)},\ldots,h^{(n_h)})\) with \(h^{(i)}\) being the number of units of the derivative \(H^{(i)}\), \(i=1,2,\ldots,n_h\).

In all our discussions, components of a portfolio are allowed to take fractional values. This is not always feasible in practice, for instance, stocks are usually traded in whole units. However, fractional values can be interpreted as proportional holdings, and a fractional component may be scaled by a suitable integer to make it into an integer.

Often it is useful in our discussions to split the portfolio into two parts, namely, the spot (or capital) market part and the derivatives market part. We use the following notations for these two parts of a portfolio

Given a market, building a portfolio involves three steps:

- Select the assets to include in the portfolio and determine their quantities.

- Plan the order in which the assets are to be traded (in some cases, the ordering may not matter).

- Execute the trading plan by buying and selling the assets in the market.

First Mrs. Sahana bought 10 shares of TCS, 50 shares of SBI, 7 shares of Bajaj Auto. After few days, she exited Bajaj Auto position fully and bought 12 shares of Reliance. Again, after few more days, she sold 5 shares of TCS and bought 8 shares of Infosys.

where 1 unit of a bond \(B_1\) is bought, 2 shares of \(S_1\) are bought, \(10\) shares of \(S_2\) are sold, and a long position in 1 contract of a future (or forward or option) \(f_1\) (say) is taken at the present time \(t=0\). A short position in \(\Pi\), denoted by \(-\Pi\), is

indicating shorting 1 unit of \(B_1\), selling 2 shares of \(S_1\), buying 10 shares of \(S_2\), and taking a short position in 1 contract of \(f_1\) at \(t=0\).

Value and Gain Processes

Once the portfolio is built, its value can be determined at every time instance.

Assume that a portfolio (denoted by \(\Pi_{t_1}\) or simply \(\Pi_1\)) is built at time \(t=t_0\) and is held until time \(t=t_1\). The portfolio value at any time \(t\in [t_0,t_1]\) is defined as

where \(S^{(i)}(t)\) denotes the per unit current market price for the asset \(S^{(i)}\) at time \(t\) and similarly for \(B^{(i)}\)'s and \(H^{(i)}\)'s. The above expression can also be written in the vector notation as

The portfolio at \(t=t_0\) out of the market considered in Example «Click Here» is

where we take \(\phi_1=1\) and \(\boldsymbol{\theta}_1 = (10,5,7,0,8)\).

We now compute the value of the portfolio at \(t_0=0\), representing the initial investment of the portfolio. We always neglect the cost associated with brokerage, taxes, and any other charges involved in maintaining the portfolio. Such a valuation is referred to as the frictionless valuation.

From the buy price of the stocks, let us take \(\boldsymbol{S}_0 = (3285, 610,2333, 0, 3588).\) Therefore the total investment in stocks is given by

For the risk-free investment we take \(B_0 = 19065\) as the initial value. Therefore, the total investment in the risk-free assets is

The initial value of the portfolio is therefore given by

After the end of one year, denoted by \(T\), it is found from the market that

The frictionless value of the portfolio (neglecting the dividend payments of the stocks) at time \(T\) is given by

A price vector \(\boldsymbol{S} = (S^{(1)}, S^{(2)}, \ldots, S^{(n)})\) at any time \(t \in [t_0, t_1]\) is a random vector and therefore, \(\boldsymbol{S}=\{\boldsymbol{S}_t\}\) is a stochastic process. Consequently, we have the value process \(V=\{V_t\}\) defined as

For a given time partition \(0=t_0 < t_1 < t_2 < \ldots,\)

- The value of the portfolio \(\Pi_1\) (created initially at time \(t_0\)) at the initial time \(t_0\) is denoted by \(V_0\). Thus,

\[ V_0 = V(\Pi_1)(t_0). \]

- The value of \(\Pi_1\) at \(t_1\) is denoted by \(V_1\). That is,

\[ V_1 = V(\Pi_1)(t_1). \]

- In general, the value of \(\Pi_k\) at \(t_k\) is denoted by \(V_k\).

Let \(\Pi_1\) be a portfolio created at time \(t_0=0\) and held until time \(t_1 > t_0\). The gain process of the portfolio is defined as

where \(\Delta\boldsymbol{S}_t = \boldsymbol{S}_t -\boldsymbol{S}_0 \) and similarly for other components.

https://www.nseindia.com/report-detail/eq\_security

Follow the notation as given in Definition «Click Here» .

Market Model

Let us start with a single step discrete capital market model which involves a probability space (\(\Omega, \mathcal{F}_*, \mathbb{P})\) on which the prices of the risky securities \(\boldsymbol{S}_1\) at time \(t_1\) are defined as non-negative random variables. Here, \(\Omega\) has a finite number of elements, \(\mathcal{F}_*\) denotes the power set of \(\Omega\) and \(\mathbb{P}\) is a suitably defined probability such that \(\mathbb{P}(\{\omega\}) > 0\), for all \(\omega\in \Omega\).

Obviously, at \(t_0=0\), we know the asset prices \(\boldsymbol{S}_0\), whereas the prices \(\boldsymbol{S}_1\) at \(t_1=T\) are unknown. Consequently, at time \(t=t_0\), a trader does not know the exact values of the asset prices \(\boldsymbol{S}_1\), but relies on the chosen probability model to quantify the uncertainty and study their potential behavior.

Consider a capital market consisting of two stocks \((B, S^{(1)}, S^{(2)})\). Let \(S^{(1)}_0=100\) and \(S^{(2)}_0=200.\) Further, assume that the price movement of one stock does not impact the price movement of the other stock.

A technical analyst gave trading recommendation at time \(t_0=0\) on these two stocks as follows:

- Buy \(S^{(1)}\) with a target of ₹ 105 per share. However, exit the position if it touches ₹ 98 per share (generally referred to as stop loss).

- Buy \(S^{(2)}\) with a target of ₹ 208 per share with a stop loss of ₹ 197 per share.

Let us denote \(S^{(1)}_u= 105\), \(S^{(1)}_d=98\), \(S^{(2)}_u= 208\), and \(S^{(2)}_d=197\).

The sample space is

Now we have to define a probability measure on the sample space \((\Omega, \mathcal{F}_*)\). There is no unique way of defining a probability. One way is the theoretical probability called the risk-neutral probability, which will be discussed later in this course. Another is the real-world probability, which is unknown. However, we can adapt to an observed probability, which can be chosen in many ways.

One naive illustration is the following: Suppose we have a data base of recommendations given by the technical analyst for past five years. Looking into this data base, let us assume that the analyst gave buy recommendations for \(S^{(k)}\) for \(N_k\) times out of which \(n_k\) number of recommendations were successful, for \(k=1,2\). Since \(S^{(1)}\) and \(S^{(2)}\) are independent, we can consider the probability model as \((\Omega, \mathcal{F}_*, \mathbb{P})\) with

where

Predictable Strategy

Since a portfolio at a time is constructed based on the observed asset prices at that time, a collection of portfolios \(\Pi:=\{\Pi_k~|~k=1,2,\ldots\}\) can be viewed as a vector-valued stochastic process in \(\mathbb{R}^{n_b+n_s+n_h}\). For each \(k\), \(\Pi_k\) denotes the portfolio created at time \(t_{k-1}\) using the information available up to time \(t_{k-1},\) and held unchanged on the interval \([t_{k-1}, t_k).\) We refer to this portfolio process as a portfolio strategy or simply a strategy.

We are interested in predictable strategy.

A stochastic process \(\{X_k~|~k=1,2,\ldots\}\) defined on a probability space \((\Omega, \mathcal{F},\mathbb{P})\) is said to be predictable with respect to a filtration \(\{\mathcal{F}_k~|~k=0,1,2,\ldots\}\) if \(X_k\) is \(\mathcal{F}_{k-1}\)-measurable, for every \(k=1,2,\ldots\).

A predictable strategy is called a trading strategy.

Our next task is to specify a market filtration, which represents the information available to traders over time. In other words, we look for a filtration with respect to which the price process \(\boldsymbol{S}=\{\boldsymbol{S}_t\}\) is adapted (see Definition «Click Here» ).

For a given stochastic process \(\boldsymbol{S}\), we can always choose a filtration which makes the process adapted. Such a filtration, the natural filtration, is already illustrated in Example «Click Here» . We can also construct natural filtration through generated \(\sigma\)-fields from random vectors.

For a given stochastic process \(\boldsymbol{S}\), the filtration defined by

is called the natural filtration for \(\boldsymbol{S}\).

where \(\mathcal{B}(\mathbb{R})\) denotes the collection of all Borel sets in \(\mathbb{R}\). Since \(S_0\) is a constant, \(\mathcal{F}_0^S = \{\emptyset, \Omega\}\), the trivial \(\sigma\)-field.

where \(\mathcal{B}(\mathbb{R})\) denotes the collection of all Borel sets in \(\mathbb{R}\).

Our next question is the following:

Is every portfolio process a predictable process with respect to the natural filtration?

Self-financing Strategy

Another important condition that we impose on a trading strategy is the self-financing condition, which rules out any infusion or withdrawal of external capital during the trading period.

A strategy \(\Pi:=\{\Pi_k~|~k=1,2,\ldots,n\}\) is said to be a self-financing strategy if

for every \(k=1,2,\ldots, n-1\).

The definitions of portfolio value and gain can be extended to strategy as follows:

- The value of a strategy at any time \(t\in [t_0, t_n]\) is defined as

\[ V_t(\Pi) = V_t(\Pi_k), \text{ if } t\in [t_{k-1}, t_k],~\text{for some}~k=1,2,\ldots, n. \]

We also use the notation \(V_t\) to denote the value of a given strategy at time \(t\).

- The gain of a strategy at any time \(t\in [t_0, t_n]\) is defined in a similar way.

Next, we recall a result from basic probability theory, which is used in Problem «Click Here» to establish the measurability properties of trading strategies.

Let \((\Omega, \mathcal{F})\) be a sample space. Suppose \(X_1, X_2, \dots, X_n: \Omega \to \mathbb{R}\) are \(\mathcal{F}\)-measurable random variables. If \(g: \mathbb{R}^n \to \mathbb{R}\) is a Borel-measurable function, then the function

is also \(\mathcal{F}\)-measurable.

Arbitrage Opportunity

An arbitrage opportunity in a market refers to the existence of a portfolio that yields a non-negative payoff with no possibility of loss and a strictly positive payoff with positive probability.

Such opportunities often arise in a market due to the mispricing of similar securities traded in different segments of the market. For theoretical flexibility, one may also include the condition that the initial value of the portfolio is zero. The concept of arbitrage is fundamental to many financial pricing models and serves as a key principle in understanding market efficiency.

Arbitrage Portfolio

Let us now formalize the concept of arbitrage with a rigorous mathematical definition. We begin by defining an arbitrage portfolio, which refers to a portfolio held from time \(0\) to time \(T\). Later, we will extend this notion to arbitrage strategies in a dynamic trading framework.

A portfolio \(\Pi\) of a market is said to be an arbitrage portfolio (or simply arbitrage) in a time period \([0,T]\), say, if it satisfies the following conditions:

- \(V(\Pi)(0) = 0,\)

- \(V(\Pi)(T)\ge 0\), \(\mathbb{P}\)-a.s. and

- \(\mathbb{P}\big(V(\Pi)(T)>0\big)>0\).

If at least one arbitrage portfolio exists in a market, then we say that the market has arbitrage opportunity. A market is said to be an arbitrage-free market or a viable market if it provides no arbitrage opportunities.

The presence of arbitrage indicates inefficiencies in the market, as rational investors would take advantage of these opportunities until the discrepancies are eliminated. In our course, we always assume that the market is viable.

Consider a hypothetical situation with two bank offers, Bank-L and Bank-D. Bank-L offers a loan at the continuously compounded rate of 8% per annum, while Bank-D offers a deposit at the rate of 9% per annum, continuously compounded.

Build a portfolio by making the following investments:

Then we can see that \(V(\Pi)(0) = 0\). After one year, the deposit in Bank-D gives

while the liability with Bank-L is

Therefore,

Assuming no credit risk, this positive gain with probability 1 implies an arbitrage opportunity in the market.

Observe that the arbitrage condition of a portfolio depends on the probability measure that we use. In the above example, we have not explicitly defined the probability measure to check the arbitrage condition because the situation is intuitively clear. However, in other scenarios, we may need to consider a suitable probability measure to verify arbitrage conditions.

Application: Forward Pricing

In this subsection, we derive a deterministic model for forward price in the simplest scenario where there are no additional costs associated with holding the underlying asset until maturity. Recall that the forward price is the delivery price the buyer has to pay to the writer to own the underlying asset at the expiration time \(t=T\), whereas no money is exchanged at the time \(t=0\) when the contract is initiated. We denote the delivery price of a contract with the expiration \(t=T\) by \(F(0,T)\). The forward price evolves in time due to ongoing trades in the forward market and fluctuations in the underlying asset price. The forward price in the market at any time \(t\in [0,T]\) is denoted by \(F(t,T)\). The return in a forward contract for the long position is defined as

We make two basic assumptions:

- Frictionless Trade: We always neglect the cost associated with brokerage, taxes, and any other charges involved in maintaining the portfolio. Such a valuation is referred to as the frictionless valuation.

- Ideal Bank: The prevailing interest rate in a risk-free investment is the same for both lending and borrowing. Such an instrument is referred to as an ideal bank. Further, we assume that this instrument can lend and borrow any amount of money.

Suppose the underlying asset involves no extra cost throughout the forward contract period. Further, assume that the market is arbitrage-free and allows short trades. Then, under continuous compounding, the forward price at any time \(t\in [0,T]\) is given by

where \(S(t)\) is the per unit spot price of the underlying asset at time \(t\) and \(r\) is the prevailing risk-free annual interest rate both for lending and borrowing.

Case 1:

Assume the contrary that \(F(0,T)>S(0)e^{rT}\). We construct a portfolio as follows:

\(~~\) asset for \(F(0,T)\) at time \(T\).

The portfolio thus constructed is denoted by the 3-tuple

where \(\phi = -1, \theta^{(1)}=1, \text{ and } h^{(1)}=-1.\)

The value of the portfolio at \(t=0\) is

The value of the portfolio \(\Pi\) at \(t=T\) is

where we have used the property \(F(T,T) = S(T)\), which holds in an arbitrage-free market (prove it).

According to our assumption, it is evident that

which happens with certainty, and therefore its probability (whichever may be the probability measure) is 1. Hence, \(\Pi\) is an arbitrage portfolio. This contradicts our assumption that there is no arbitrage opportunity available in the market.

Case 2:

On the other hand, assume that \(F(0,T) < S(0)e^{rT}\). We again can construct an arbitrage portfolio and contradict the viable market assumption. The proof is left as an exercise.

The model suggested in Theorem «Click Here» give a fair value for a forward price given a prevailing interest rate scheme.

- The interest rate is fixed and known at time \(t\).

- The underlying asset price \(S(t)\) is known at time \(t\).

These assumptions completely neglect the randomness in the pricing process, and the model can only be used with \(t\) as the present time. However, a more realistic model should consider \(r\) as a random variable. If we want to use this model with \(t=0\) as the present time and \(t\in (0,T]\) as a future time, then we have to include stochastic models that simulate \(r_t\) and \(S_t\) as random variables.

\(~\)

Law of One Price

The derivative pricing models we derive in later chapters rely on assuming the market is viable. There are at least two methods that we can use to derive these models:

- Arbitrage Portfolio Approach: First, propose a fair price for the contract and then justify it by showing that any deviation of the proposed fair price can lead to the construction of an arbitrage portfolio contradicting the viable market assumption; and

- Replicating Portfolio Approach: This method involves constructing a portfolio that generates the same payoff as the required instrument at a future time and then applying the law of one price.

The law of one price is a fundamental principle in economics and finance, which states that identical assets should be priced consistently across different markets in an efficient market scenario. We extend this economic principle to a portfolio and give a mathematical framework to it.

Two portfolios \(\Pi_1\) and \(\Pi_2\) defined on a time interval \([0,T]\) are said to satisfy the law of one price (LOP) if

then

for all \(t\in [0,T]\).

We now prove a sufficient condition for a pair of portfolios to satisfy the law of one price.

Arbitrage Strategy

Observe that Definition «Click Here» introduced the concept of arbitrage for a static portfolio. This can be extended to a arbitrage strategy to incorporate dynamic arbitrage.

A strategy \(\Pi:=\{\Pi_k~|~k=1,2,\ldots,n-1\}\) in a market is said to be an arbitrage strategy or (simply arbitrage) if its value process satisfies the following conditions:

- \(V_0(\Pi) = 0,\)

- \(V_k(\Pi_{k}) = V_{k}(\Pi_{k+1}),\) for every \(k=1,2,\ldots, n-1\),

- \(V_n(\Pi)\ge 0\), \(\mathbb{P}\)-a.s. and

- \(\mathbb{P}\big(V_n(\Pi)>0\big)>0\).

Thus, a market is said to have arbitrage opportunity if there exists a self-financing strategy \(\Pi\) in the market such that all the conditions in Definition «Click Here» hold now for the value process of the strategy \(\Pi\).

The concept of the law of one price, discussed in Section «Click Here», can also be extended to self-financing strategies.

Application: Future Contracts

A future contract is a derivative instrument that falls under the category of noncontingent claims in financial markets. These contracts represent agreements to buy or sell an underlying asset at a predetermined price on a specified future date, just like how forward contracts function.

Commonly traded underlying assets in futures contracts include:

- Commodities such as agricultural products (e.g., wheat, corn, soybeans), energy products (like crude oil, natural gas), and metals (like gold, silver);

- Financial instruments such as stock indices, stocks and interest rates; and

- Currencies.

Let us take the period of a future contract as the interval \([0,T]\), where \(t=0\) marks the moment at which the contract is traded (exchanged between the writer/seller and the holder/buyer) and \(t=T\) is the expiration time (the future market closing time on the expiration date).

A futures market quotes a price for the underlying asset at every trading time \( t\in [0,T],\) referred to as the future price or the delivery price or the settle price, denote by \(f(t,T)\). This price represents the value at which the underlying asset is delivered at the expiration time \(T\). The price of the same asset at the spot market is often different from the future price, called the spot price and is denoted by \(S(t)\). Understanding the relationship between the future price and the spot price is important and is the primary focus of this section.

The basic working mechanism of futures contracts is similar to forward contracts. However, there are a few key distinctions between them:

- Futures contracts are traded on organized exchanges, whereas forwards are typically traded over-the-counter (OTC).

- Exchanges settle futures contracts on a daily basis through a process called marking to market, which means that the value of the contract is adjusted daily based on current market prices. In contrast, forwards only have physical settlements on the expiration date, where the underlying asset is delivered or exchanged.

Marking to Market

In a futures market, marking to market (MTM) refers to the process of adjusting the value of a futures contract based on the current future price of the underlying asset. This adjustment occurs daily, typically at the end of each trading day. MTM plays a crucial role in managing counterparty risk by ensuring that losses are immediately covered, thus reducing the risk of default.

First, let's explore how the MTM process operates in an exchange market. Consider a partitioned \(\boldsymbol{t} = (t_0=0, t_1, \ldots, t_{n-1}, t_{n}=T)\) of the interval \([0,T]\), where each \(t_k\), for \(k=1,2,\ldots, n\), is the closing time of the market on the \(k^{\rm th}\) trading day of the future contract.

This ensures that gains or losses are settled daily to maintain fair and transparent market conditions.

Note that, unlike coupon bonds where we get a deterministic cash flow stream, in futures, we get a random cash flow stream.

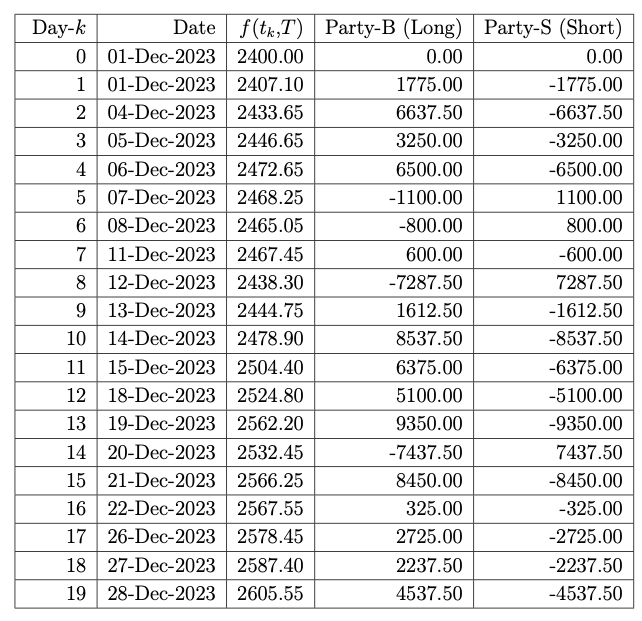

Let us illustrate the marking to market process in the following example:

Assuming a margin requirement of 10% of the total trade value at expiry, the exchange requires an initial margin of ₹ 60000 from each party. The marking to market cash flows for Party-B and Party-S are shown in \tabl{marking.market.tb}, representing the daily adjustments in their margin accounts based on changes in the future price. We refer the table as the marking to market table.

Assume that a party gets maintenance margin call when the margin account goes below 50% of the requirement. Then, we see that the margin deposit of Party-S on 18\(^{\rm th}\) December evening had gone below 50% of the total margin requirement. Hence Party-S would have got a maintenance margin call from the exchange on this day to retain the position on the following day.

The marking to market process continues in a contract until either the expiry date or one of the parties leaves the position by taking an equal and opposite position in the contract. For instance, if Party-B (long) wants to close the position in the contract before expiry, Party-B can enter into a contract of equal quantity (250 in the above example) where the position is a short position. This can be achieved by selling a contract of equal quantity of the same asset with an expiration date \(T\) in the future market. Similarly, if Party-S (short) wants to close the position, Party-S has to buy the same contract (with the same expiration date and asset) of equal quantity. Closing a contract is referred to as offset (or square off) the position.

Pricing Model

We now establish the futures pricing model assuming a constant prevailing interest rate throughout the futures contract period. We justify the model using replicating portfolio approach discussed in Section «Click Here». Since the basic mechanism of a future contract is the same as a forward contract, we construct two strategies, one with a forward contract and the other with an equivalent future contract, so that both lead to the same future value and are deterministic.

Recall that the future price \(f(t,T)\) (see Definition «Click Here» ) of the underlying asset generally differs from the spot price \(S(t)\). Similar to forward contracts, the future price \(f(t,T)\) tends to converge to \(S(T)\) as \(t \rightarrow T\), with \(f(T,T) = S(T)\).

where \(T\) is the expiration time of the contract.

Construct a portfolio \(\Pi_F\) with the following trades:

- Take a long forward position with forward price \(F(0,T)\) (no cost involved).

- Invest \(e^{-rT}F(0,T)\) amount in a risk free asset.

At time \(T\), the value is

Trades based on future:

For the sake of simplicity, we assume that marking to market is performed at just two intermediate time instances, \(0 < t_1 < t_2 < T\). Thus, we consider the partition \(\{t_0=0, t_1, t_2, t_3=T\}\) for the interval \([0, T]\). Note that in futures trading, each partition point \(t_k\) corresponds to a trading day, and therefore, the number of partitions should be equal to the number of trading days until the future expiration time. The argument below can readily be extended to cover more frequent marking to market.

At time \(t_0=0\): Construct a portfolio \(\Pi_{{f}_1}\) with the following trades:

- Open a fraction of \(e^{-r(T-t_1)}\) units long in future (no cost involved).

- Invest the amount \(e^{-rT}f(0,T)\) in a risk free interest rate investment (this investment will grow to \(f(0,T)\) at time \(T\)).

At time \(t_1\): Make the following adjustments in \(\Pi_{{f}_1}\) to make a new portfolio \(\Pi_{{f}_2}\):

- Receive (or pay) the amount \(e^{-r(T-t_1)}(f(t_1,T)-f(0,T))\) as a result of marking to market.

- Invest (or borrow, depending on the sign) \(e^{-r(T-t_1)}(f(t_1,T)-f(0,T))\) in a risk free interest rate investment (this amount will be \(f(t_1,T)-f(0,T)\) at time \(T\)).

- Increase the long futures position to \(e^{-r(T-t_2)}\) (no cost involved).

At time \(t_2\): Make the following adjustments in \(\Pi_{{f}_2}\) to make a new portfolio \(\Pi_{{f}_3}\):

- Receive (or pay) the amount \(e^{-r(T-t_2)}(f(t_2,T)-f(t_1,T))\) as a result of marking to market.

- Invest (or borrow, depending on the sign) \(e^{-r(T-t_2)}(f(t_2,T)-f(t_1,T))\) in a risk free interest rate investment (this amount will be \(f(t_2,T)-f(t_1,T)\) at time \(T\)).

- Increase the long futures position to 1 unit (no cost involved).

At time \(T\): The value of \(\Pi_{{f}_3}\) at \(t_3=T\) is

Hence, the final wealth at maturity is \(S(T)\).

Observe that, the initial investment is \(e^{-rT}f(0,T)\) and the closing value is \(S(T)\). Thus, both the forward portfolio \(\Pi_F\) and the sequence of future portfolios \(\Pi_f:=\{\Pi_{{f}_k}: k = 1,2,3\}\) generate the wealth worth \(S(T)\) at time \(T\). Since, the market is assumed to be no-arbitrage, by Lemma «Click Here» , the law of one price holds for both \(\Pi_F\) and \(\Pi_f\). Hence, we have

This completes the proof.

assuming that the underlying asset does not involve any extra costs or dividends. Deviation of futures prices from this model is typically attributed to anticipated changes in interest rates.

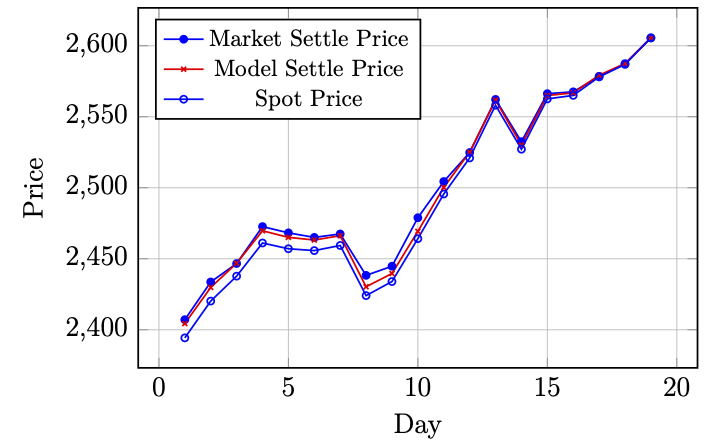

The figure below depicts the comparison of the market future price (settle price) with the model price obtained using the above formula with \(r=0.085\) and the spot price \(S\). The Reliance stock is used as the underlying asset in the depicted comparison result, where the future is for December 2023, spanning from the 1\(^{\text{st}}\) to the 28\(^{\text{th}}\) of December 2023 (also refer to Example «Click Here» ).

- the asset price grows more than the prevailing interest rate;

- the asset price grows, but less than the prevailing interest rate; and

- the asset price decreases.

Date, Settle Price, Model Price, Spot Price

Here, model price is obtained using the formula given in Remark «Click Here» , where \(r\) is taken as an input, whereas \(T\) is obtain by the code itself. Download the input csv file from the following link: NSE India Contract-wise Price Archives